Life Insurance

Protect loved ones from your loss

This provides protection against financial loss that would result from the premature death of an insured. The named beneficiary receives the proceeds and is thereby safeguarded from the financial impact of the death of the insured.

Why choose Covenant Insurance Brokers?

WHY DO YOU NEED LIFE INSURANCE?

A life insurance policy is a critical part of prudent financial planning. In the event of critical illness, disability or death, life insurance provides a safety net for you and your family, enabling them to maintain their lifestyle in a dignified manner.

Our life insurance providers, like Guardian Life, offer a range of policy options to meet your specific needs. There are Whole Life insurance policies – which provide coverage for the “whole” of your life, as well as Term insurance policies which provide coverage over a fixed period and can be renewed. Give us a call today for info, policies can be tailor made for your life’s changing needs.

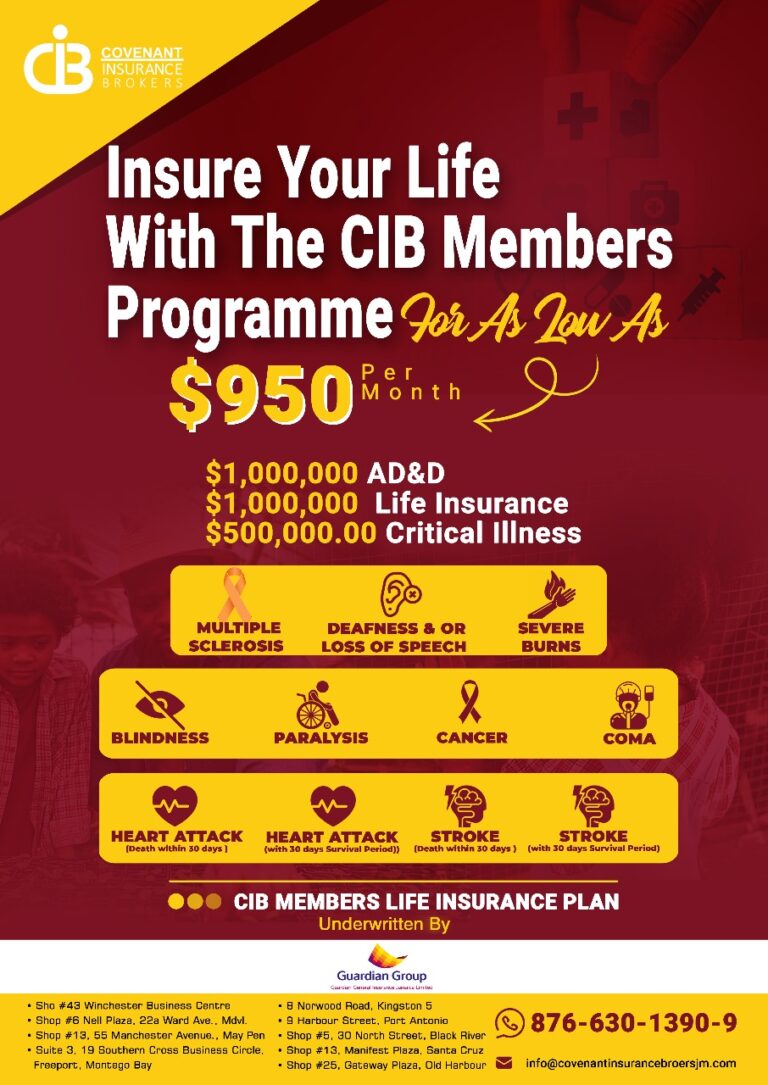

CIB Life Members Plan

Meet The Team

Allistere Benson

Life Insurance Advisor

Jehnelle Campbell

Financial Advisor

Nickeba Dunkley

Life Unit Manager